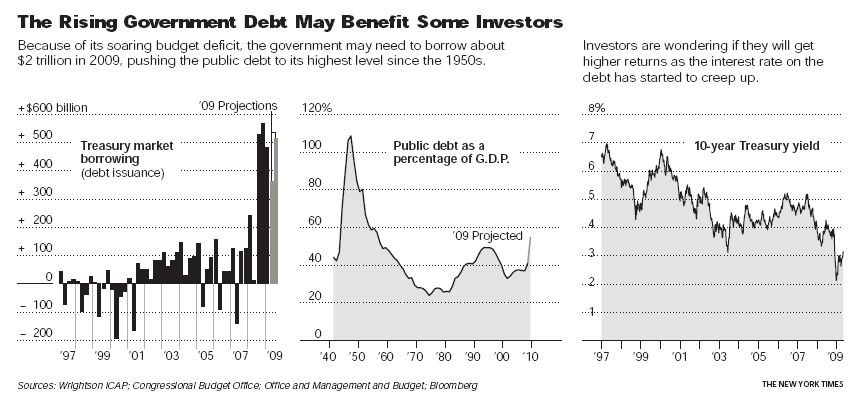

Foreigners Continue to Fund US Trade Deficit

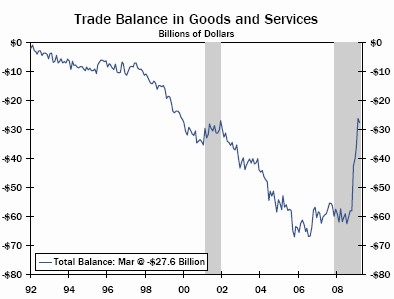

Economists generally and Dollar bears specifically both love to harp on the perennial US trade imbalance. Despite the halving of the trade deficit (reported by the Forex Blog last week), the gap between exports and imports remains sizable; it is projected at about a $350 Billion for 2009.

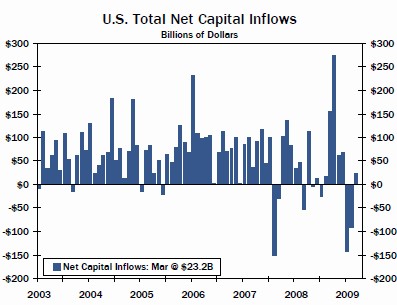

The more important data point, however, concerns capital flows. This is applies mainly currency traders, which are less intrinsically worried about the US trade imbalance than how the rest of the world feels about supporting such a balance. For example, if the entire trade deficit is recycled (i.e. invested) back into the US, than theoretically a trade deficit presents nothing to worry about, at least not in the short run. [Of course, such a trend may not be sustainable for the long-term, but that is outside the purview of this post].

The Dollar’s de facto role as the world’s reserve currency has historically ensured that this has been the case. This phenomena has even been strengthened by the credit crisis, as the initial spike in risk aversion generated a steady demand for Dollar-denominated assets. However, there was concern that this demand was leveling off over the last few months as risk aversion ebbed, and foreigners collectively sold a net $95 Billion worth of American assets. Over this period, the Dollar by no coincidence has declined across the board, against both emerging market currencies as well as the majors.

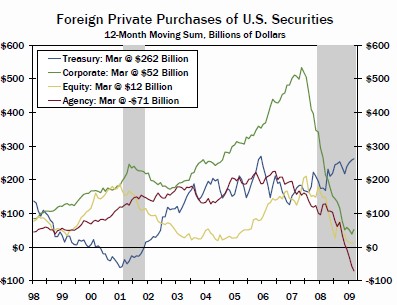

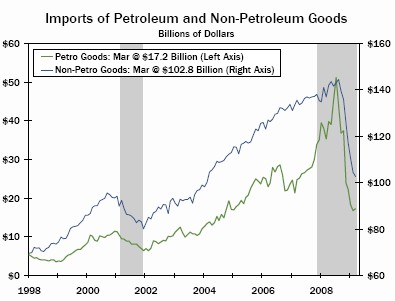

In March – the most recent month for which data is available – this trend reversed itself. Net capital inflows totalled $23.2 Billion, close to the $27 Billion US trade deficit. Especially surprising is that foreign demand for US Treasury securities remained strong – to the tune of $55 Billion – despite low yields. Moreover, the two most important customers both chipped in: “China, the largest holder of U.S. Treasury securities, increased its holdings of government bonds further in March to $767.9 billion. In February, it held $744.2 billion. Japan’s Treasury holdings stood at $686.7 billion in March, compared with $661.9 billion in the prior month.”

Even demand for equity securities remained strong, as foreigners purchased $12 Billion in March alone. Foreign demand and the rising stock market are probably now reinforcing each other. Meanwhile, US investors collectively continue to pull money from abroad and return it to the US; over $100 Billion has already been returned to the US in this way.

Taken at face value, this is certainly good news. Given all the bad news, the fact that capital is still flowing into the US is worth celebrating. At the same time, the fact that the Dollar continues to fall suggests that this more to the story than meets the eye…

Note: Both Charts courtesy of International Business Times.

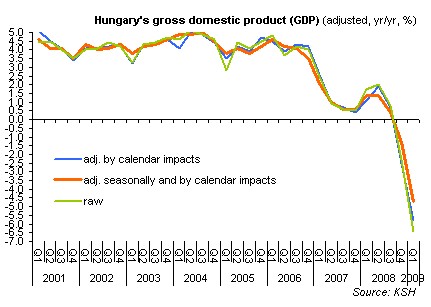

After all, Canadian economic fundamentals remain abysmal by any standards, because of the collapse in commodity prices and a decline in exports to its biggest trade partner, the US. “Canada’s central bank has said the country’s gross domestic product fell 7.3 percent in the first three months of 2009, dropping at the

After all, Canadian economic fundamentals remain abysmal by any standards, because of the collapse in commodity prices and a decline in exports to its biggest trade partner, the US. “Canada’s central bank has said the country’s gross domestic product fell 7.3 percent in the first three months of 2009, dropping at the

In other words, investors are allocating capital on the basis of risk, rather than in accordance with (economic) fundamentals. For example, “ICE’s Dollar Index and crude oil have a

In other words, investors are allocating capital on the basis of risk, rather than in accordance with (economic) fundamentals. For example, “ICE’s Dollar Index and crude oil have a

Now, with a global stock market rally underway and a modest economic recovery taking shape on the horizon, the Singapore Dollar has quickly erased almost half of its slide. The Central Bank naturally, is alarmed, and is threatening to intervene. While the MAS, itself, has thus far denied such a possibility, insiders suggested that “The Monetary Authority of Singapore will buy the U.S. dollar “‘f it falls below S$1.4700, around S$1.4690…’ [which] roughly equates with the strong end of the undisclosed

Now, with a global stock market rally underway and a modest economic recovery taking shape on the horizon, the Singapore Dollar has quickly erased almost half of its slide. The Central Bank naturally, is alarmed, and is threatening to intervene. While the MAS, itself, has thus far denied such a possibility, insiders suggested that “The Monetary Authority of Singapore will buy the U.S. dollar “‘f it falls below S$1.4700, around S$1.4690…’ [which] roughly equates with the strong end of the undisclosed

In fact, the Bank of England just announced a huge expansion in its program, increasing total debt buying (i.e. money printing) by $50 Billion. One analyst summarized the impact of this announcement on forex markets as follows: “The Bank of England’s aggressive stance with regard to quantitative easing is adding to concern about the economy and that is negative for sterling.” Not much nuance there….

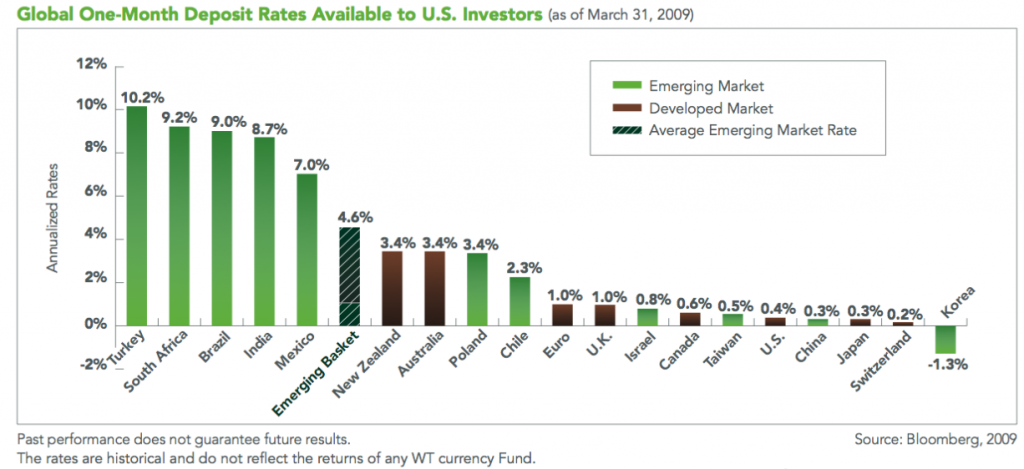

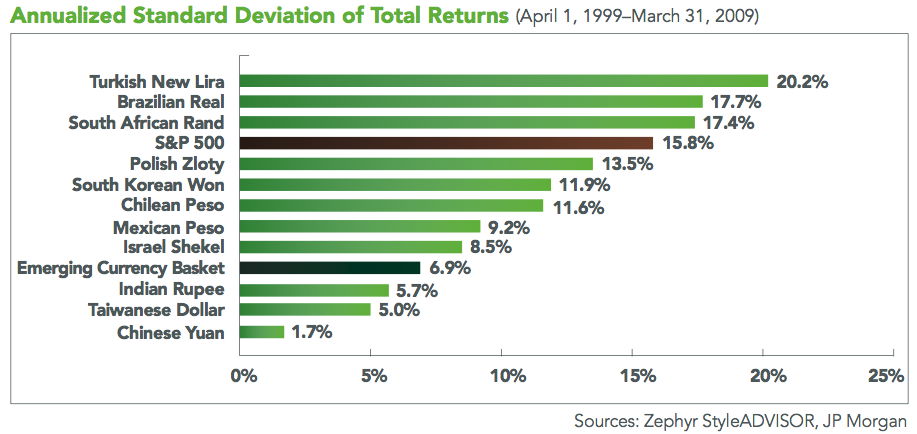

In fact, the Bank of England just announced a huge expansion in its program, increasing total debt buying (i.e. money printing) by $50 Billion. One analyst summarized the impact of this announcement on forex markets as follows: “The Bank of England’s aggressive stance with regard to quantitative easing is adding to concern about the economy and that is negative for sterling.” Not much nuance there…. Chosen from three regions (Latin America, Africa/Europe/Middle East, and Asia), the inaugural 11 currencies are as follows: Brazilian real, Chinese yuan, Chilean peso, Indian rupee, Israeli shekel, Mexican peso, Polish zloty, South African rand, South Korean won, Taiwanese dollar and Turkish new lira. According to WisdomTree, these currencies were selected not necessarily for economic reasons, but rather because of their relatively high liquidity and low correlation with each other. In addition, “The selected currencies are

Chosen from three regions (Latin America, Africa/Europe/Middle East, and Asia), the inaugural 11 currencies are as follows: Brazilian real, Chinese yuan, Chilean peso, Indian rupee, Israeli shekel, Mexican peso, Polish zloty, South African rand, South Korean won, Taiwanese dollar and Turkish new lira. According to WisdomTree, these currencies were selected not necessarily for economic reasons, but rather because of their relatively high liquidity and low correlation with each other. In addition, “The selected currencies are

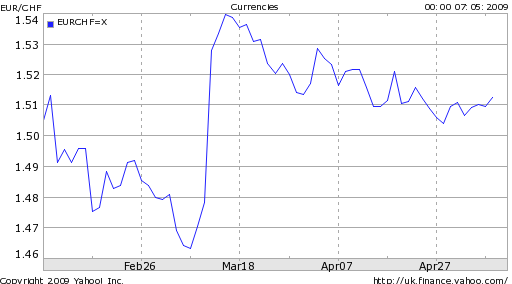

It was unclear whether the Central Bank had chosen a magic threshold, such that a rise by the Franc above which would trigger a sale of Francs in the open market. Earlier in the week, one analyst asserted, “With the euro/franc exchange rate almost at pre-intervention levels – the euro jumped to a level above CHF1.52 after the SNB intervention in March from CHF1.4843 before the announcement – the stage is set for the SNB to

It was unclear whether the Central Bank had chosen a magic threshold, such that a rise by the Franc above which would trigger a sale of Francs in the open market. Earlier in the week, one analyst asserted, “With the euro/franc exchange rate almost at pre-intervention levels – the euro jumped to a level above CHF1.52 after the SNB intervention in March from CHF1.4843 before the announcement – the stage is set for the SNB to

Nonetheless, the Fed made a point of emphasizing that the economy seems to be stabilizing: “Information received since the Federal Open Market Committee met in March indicates that the

Nonetheless, the Fed made a point of emphasizing that the economy seems to be stabilizing: “Information received since the Federal Open Market Committee met in March indicates that the