February 9th 2010

Chinese Yuan Expectations Revised Downwards

Last month, I reported on how anticipation is (was) building towards a revaluation of the Chinese Yuan (RMB), confidently stating that “The only questions are when, how and to what extent.” While I’m not ready to recant that prediction just yet, I may have to temper it somewhat.

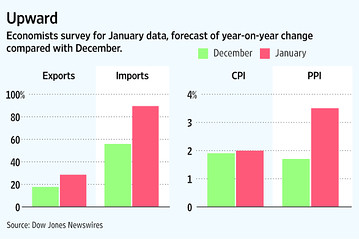

On the one hand, the case for RMB revaluation is stronger than ever. Among large economies, China’s economy is by far the strongest in the world, clocking in GDP of close to 2009% while most other economies were lucky to “break even.” Meanwhile, its export sector – supporting which is the primary purpose of the RMB peg – is once again robust, having recovered almost completely from a drop-off in demand in 2008 and the first half of 2009. In fact, exports grew by 30% in January, on a year-over-year basis. China’s share of global exports is now an impressive 9%, up from only 7% in 2006. From an economic standpoint, then, the case for an artificially cheap currency is no longer easy to make.

At the same time, the RMB peg is contributing to bubbles in property and other asset markets. That’s because the Central Bank of China has been forced to mirror the monetary policy of the Fed, as a significant interest rate differential would stimulate uncontrollable capital inflows from yield-hungry investors. While the US can still handle interest rates of close to 0%, China’s economy clearly can not. Thus, consumer prices are slowly creeping up, and property prices are soaring. The most effective (and perhaps the only) way for China to contain both consumer price and asset price inflation is to hike interest rates, which which in turn, would necessitate a rise in the RMB.

There is also the notion that the peg is becoming increasingly costly to maintain. China’s forex reserves already total $2.4 Trillion, and each Dollar that it adds will be worth less if/when it ultimately allows the RMB to appreciate further. In addition, China’s economic policymakers continue to fret about its exposure to the fiscal problems of the US, with one pointing out that, “China has effectively been kidnapped by U.S. debt.” Of course, they no doubt realize that there isn’t a better option at this point; its attempt to diversify its reserves into other assets proved disastrous. The solution to both of these problems, of course, would simply be to allow the Yuan to fluctuate based on market forces, or at least for it to resume its upward path of appreciation.

Political pressure on China to revalue, meanwhile, is even stronger than it was last month. While not invoking China by name, President Obama has been increasingly blunt about the need to pressure it on the RMB: “One of the challenges that we’ve got to address internationally is currency rates and how they match up to make sure that our goods are not artificially inflated in price and their goods are artificially deflated in price.” In addition, rumor has it that the Treasury Department could finally label China as a “currency manipulator” in its next report, which would allow Congress to impose punitive trade sanctions.

Developing countries, which now account for a majority of China’s exports, are also increasingly unhappy with the status quo. The peg to the Dollar caused many emerging market currencies to appreciate rapidly against the Yuan in 2009, and there is evidence that many of their trade imbalances with China are rapidly worsening, “with exports to India, Brazil, Indonesia and Mexico growing by 30% to 50% in recent months.” As one analyst pointed out, however, the potential backlash from this development could be massive: “It’s one thing to produce job losses in the U.S., but it’s another to produce job losses in Pakistan,’ with which China has close military ties.”

On the other hand, however, is China’s massive reluctance to allow the Yuan to appreciate. Part of this is related to face; with the US and other countries stepping up pressure on a number of fronts, China’s leaders don’t want to be seen as weak, and could act contrary to their own interests if it thinks it can earn political points in the process. “China is unlikely to make significant concessions to U.S. pressure on the yuan, particularly now when the two countries are involved in a range of disputes, including U.S. arms sales to Taiwan,” explained one analyst. More importantly, the leadership is nervous that the nascent economic recovery is not sufficiently grounded for the peg to be loosened. While 9% growth in most other economies would be cause for celebration, in China, it is being interpreted as evidence of fragility.

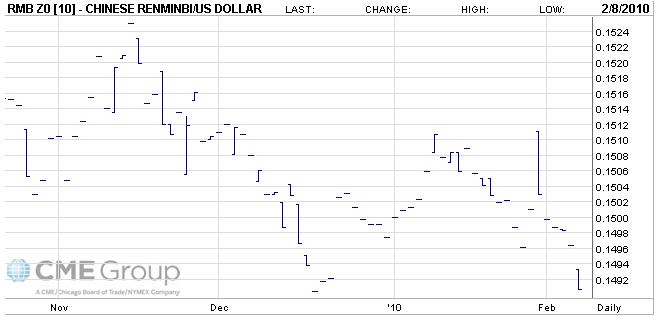

There you have it. Reason on one side, and politics on the other. Unfortunately, it seems that politics always triumphs in the end. Despite Treasury Secretary Geithner’s recent assertions that the RMB will rise soon, investors know that China ultimately calls the shots: “When it comes to the exchange rate, China’s main consideration is China’s own stable economic growth and the structural adjustment of its economy. Foreign pressure is only a secondary consideration.” In short, the RMB is now projected to appreciate only 2% in 2010, according to currency futures, compared to 3.5% last month.