April 16th 2010

Inflation: Much Ado about Nothing?

One of the cornerstones of exchange rate theory is that currencies rise and fall in accordance with inflation differentials. All else being equal, if US inflation averages 5% per annum and EU inflation averages 0% per annum, then we would expect the Euro to appreciate (or the Dollar to depreciate, depending on how you look at it) by 5% against the Dollar on an annualized basis. If only it were that simple…

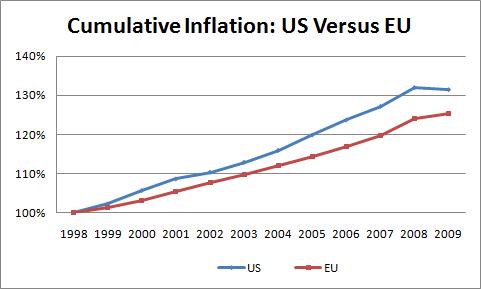

You can see from the chart below that since the introduction of the Euro, inflation in the US has slightly outpaced Eurozone inflation (by about 5% on a cumulative basis). Over that same time period, the Euro first appreciated from slightly below parity with the US Dollar to $1.60, and then fell back to the current level of around $1.35. It’s clear (from the current sovereign debt crisis if nothing else) that the EUR/USD exchange rate, then, cannot be explained entirely by the theory of purchasing power parity.

Still, insofar as inflation bears on interest rates and can be a consequence of economic overheating or excessive government spending, it is something that must be heeded. On that note, after a dis-inflationary 2009, prices in the US are once again rising in 2010, and inflation is projected to finish the year around 2%.

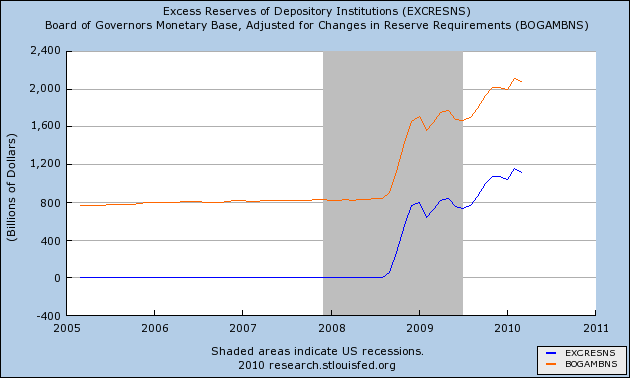

Over the longer term, there is a tremendous amount of uncertainty regarding US inflation, for a couple reasons. The first is related to the Fed’s quantitative easing program, which pumped more than $1 Trillion into credit markets. While the Fed has basically stopped its asset purchases, all of this printed money is still technically in circulation, and some inflation hawks think it represents a ticking inflation time bomb. Doves respond that the Fed will withdraw these funds before they become inflationary, and that besides, most of the funds are actually being held by commercial banks in the form of excess reserves. (This notion is in fact born out by the chart below).

The second potential driver of inflation is the skyrocketing national debt. While US budget deficits have long been the norm, they have grown alarmingly high in the past few years and are projected to remain high for at least the next decade. Beyond that, the US faces up to $70 Trillion in unfunded entitlement liabilities, which means that net debt will probably grow before it can fall. Hopefully, the US economy will outpace the national debt and/or foreign Central Banks continue to buy Treasury securities in bulk. The alternative would be wholesale money printing (to deflate the debt) and hyperinflation.

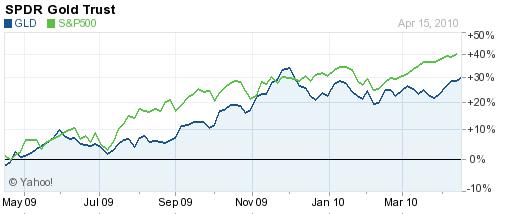

Yields on both 10-year and 30-year Treasury securities remain enviably low, which means that buyers aren’t bracing for hyperinflation just yet. In addition, while gold continues to attract buyers despite record high prices, its rise has been closely tied to the performance of the stock market, which means that investors are currently using it to bet on economic recovery, rather than as a hedge against inflation.

In short, inflation in the US certainly remains a real possibility. At this point, however, it remains too hazy to be actionable, and the forex markets will probably wait for more information before pricing it into the Dollar.