January 7th 2010

The Dollar in 2010

I thought it would be fitting to follow up my last post (Forex in 2009: A Year in Review), with one that looked forward. And what better way to do that then by squarely examining the US Dollar, which is still the undisputed heavyweight champion of forex markets, and from which most other forex trends can be ascertained and comprehended.

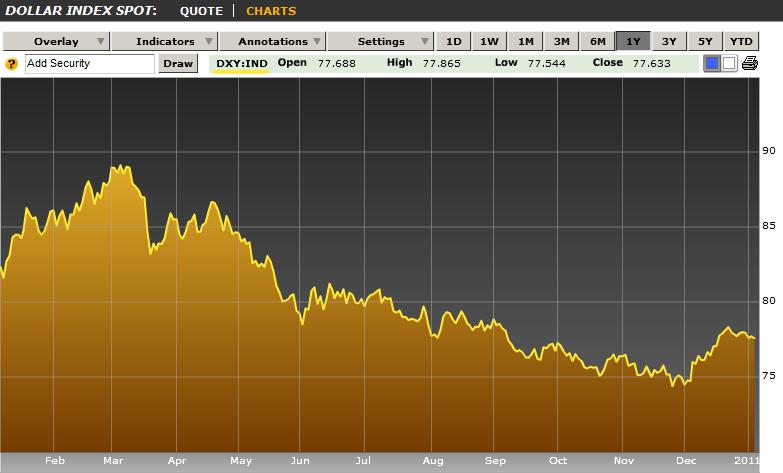

December (I know I said I wouldn’t look backwards, but come on, a little context is necessary here…) was the best month for the Dollar in 2009. From December 1 to December 31, it rose 4.7% against the Euro and 7% against the Yen, as part of an overall 4.8% appreciation against a basket of the world’s six other major currencies. “The dollar rally which has taken place in December is significant in that it has brought an end to the powerful downtrend which had been in place since March following the Fed’s decision to begin quantitative easing,” summarizes one analyst. As a result of the Dollar’s strong turnaround in December (and the forgotten fact that it actually appreciated in the beginning of last year), the broadly weighted Dollar Index finished 2009 down a modest 4%.

Analysts summarized this turnaround using a few main paradigms. The first was that logic had returned to the forex markets, such that the negative correlation between equities (which serve as a broad proxy for risk sensitivity) and the Dollar had broken down [See earlier post: “Logic” Returns to the Forex Markets, Benefiting the Dollar]. As a result, good economic news was once again good for the Dollar. The second interpretation was a direct contradiction of the first, and argued that the Dubai debt bomb, coupled with credit scares in Europe, had in fact increased risk aversion, and reinforced the notion that the Dollar is still a safe haven [Edward Hugh mentioned this in my interview of him]. The third theory represents a slight twist on the first one- that concern over Fed interest rate hikes will shift interest rate differentials and cause the Dollar carry trade to break down. Technical analysts, meanwhile, argue that the Dollar had been oversold, and that the year-end rally was merely a product of the closing of short positions and profit-taking.

The key to predicting how the Dollar will perform in 2010, then, largely rests in correctly discerning which paradigm currently underlies the forex markets. Let’s begin by comparing the first possibility – that good economic news will be good for the Dollar – to its antithesis – that the Dollar remains the safe havens. I think two WSJ headlines can shed some light on which interpretation is more accurate: Dollar Rises On Lower Demand For Riskier Assets and Dollar Slumps As Investors Snap Up Risky Assets. In other words, the market logic is that the Dollar is still a safe-haven currency, to the chagrin of market fundamentalists.

While there are certainly “naysayer” analysts that think the US stocks will soon outpace their counterparts abroad (namely in emerging markets), such a view can best be ascribed to the minority. The majority, then, believes that good economic news (from the US, or anywhere else from that matter) is a sign that risk-taking is relatively less risky, and will lead to capital flight from the US. In short, “It’s too early to dismiss the negative correlation between equities markets and the dollar, i.e., when risk appetite declines, that still seems to favor the dollar even though we’ve seen a slight decoupling from that in early December.”

With regard to the notion that the Dollar is being driven by expectations that the Fed will tighten monetary policy at some point in 2010, that seems to have some traction. The markets have priced in a 60% possibility of a Fed rate hike by June, and a majority of economists (9 out of 15 surveyed) think that the Federal Funds rate will be higher at the end of the year. This optimism is a product of the last month, which saw strong improvements in non-farm payrolls, housing sales, durable goods orders, ISM supply index, and more. Some of these indicators are now at their highest levels since 2006; “That speaks better about the health of the U.S. economy and that could help move up the timetable for the Fed to boost interest rates,” goes the accompanying logic.

That investors believe the Fed will hike interest rates and that it will be good for the Dollar is not so much in dispute. Whether investors are right about rate hikes, on the other hand, is less certain. To be sure, momentum is growing in the US as the economy shifts from recession to growth. While current data is unambiguous in this regard, the future is less certain. A vocal minority of analysts argues that the apparent stabilization is largely due to government incentives. When these expire, then, the result could be a double dip in housing prices, and a second act in the economic downturn.

The result, of course, would be a delay and/or slowing in the pace of Fed rate hikes. Some economists predict that that Fed will indeed hike rates in 2010, but only incrementally. Others have argued that it won’t be until 2012 that the Fed lifts its benchmark FFR from the current level of approximately 0%. Instead, the Fed will first move to withdraw some of the liquidity that it unleashed over the last two years, of which an estimated $1.1 Trillion still remains “in play.” Such would be directed primarily at heading off inflation, and wouldn’t do much for the Dollar.

Regardless, the implication is clear: “The fate of the dollar is in the hands of Ben Bernanke. If he begins the exit process and starts to raise interest rates, the dollar will perform okay this year.” If he stalls, and investors accept that they may have gotten ahead of themselves, well, 2010 – especially the second half – could be a sorry year for the Dollar.

January 8th, 2010 at 12:21 am

A very interesting observation. Ths US economics fundementals is still weak as far as , the WAR in IRAQ, AFGHANISTAN and most probably IRAN are concern. These wars drained the US Economy and it affect its allies as well. Back at home, the Fed Reserve are giving out goodies in support of Ben Bernanke second term in Fed Reserve. What is going on is a short terms gains with a huge iceberg waiting to hit the US economy from the bottom. The fact that the US Dollar is dependent on positive economic news is a real indicator that investor does not have any confidence in the DOLLAR on its own. The herd is moving with dollar apparently based on economic indicators taking advantage of the short term effect. That affect is beginning to wade off as for the past 2 weeks, positive news does not really move the DOLLAR that far…Today will be a decisive day for the whole scam to be out in the open…Employment data is no indicator for an overall economic health of a nation. The US expenditure, greatly overwhlmes its income..Subsidizing the WAR in the Middle East alone is killing its economy…In the home ground, if the income data shows improvement but yet still the expediture is far more bigger which creates huge deficit in the US economy…For the US economy to recover , it must first STOP the WAR in the Middle East…Restructure its banking system…Generate income through genuine business endeavour and reducing of its product and services..The next bubble to explode is the derivaties market and and such, the US Dollar is a determinant for a time bomb waiting to explode..Seek ye the truth and the truth shall set you free and apparently no one listen to Jesus and I am a Muslim saying it…Good Luck..

January 10th, 2010 at 8:59 pm

Great post. I was wondering for a little while why the USD skyrocketed to the initial economic decline and now goes down when there is bad economic news. I wonder at what point the paradigm shifted. The jobs report that just came out sent the dollar plummeting again.

I just figured that the US economy is recovering slower than the rest of the world and that emerging markets is somewhat stable again, enough for bad economic news in the US not to send investors to take refuge in the USD.