October 16th 2009

Japan Flip-Flops on Forex Intervention

In my report on last month’s Japanese election, I noted that the newly-appointed Japanese finance minister, Hirohisa Fujii, had spoken out against forex intervention. With that, it seemed the matter was closed.

But not so fast! Over the following few weeks, Fujii (as well other members of the new administration) moved to clarify his position, backtracking, sidestepping, contradicting, but never going forward. The following is a summary of selected remarks, beginning with the original statement against intervention and ending in what seems like a promise to intervene:

September 15: “I basically believe that, in principle, it’s not right for the government to intervene in the free-market economy using its money, either in stock or foreign-exchange markets.”

September 27: [The Yen’s rise is] “not abnormal…in terms of trends.”

September 28: “That’s not to say I approve of the yen’s rise.”

September 28: “I don’t think it is proper for the government to intervene in the markets arbitrarily.”

September 29: “If the currency market moves abnormally, we may take necessary steps in the national interest.”

October 3: “As I have said in Tokyo, we will take appropriate steps if one-sided movements become excessive.”

October 5: “If currencies show some excessive moves in a biased direction, we will take action.”

Confused? I know I am. Is it possible to glean any semblance of meaning from these remarks? Summarized one columnist, “Hirohisa Fujii has gone through several cycles of remarks that first appeared to favor a strong yen and then seemed to backpedal after markets took him at his word and sent the Japanese currency soaring.”

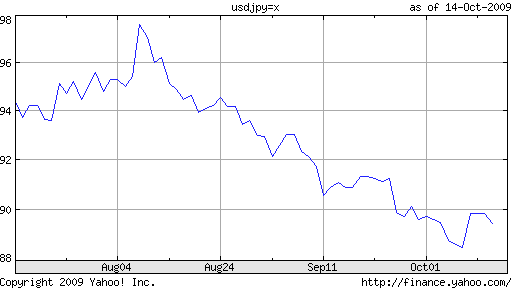

I think this encapsulates the regret that Minister Fujii must have felt, after his original comments were taken a little too seriously. In hindsight, it appears that Fujii attempted to convey the new administration’s stance on forex, in a nutshell, and certainly didn’t expect that investors would run wild and send the Yen up another 4%, bringing the year-to-date appreciation against the Dollar to 15%. In the words of the same columnist cited above, “Japan’s finance minister has been rudely reminded of the cardinal rule when speaking to markets — less is more.”

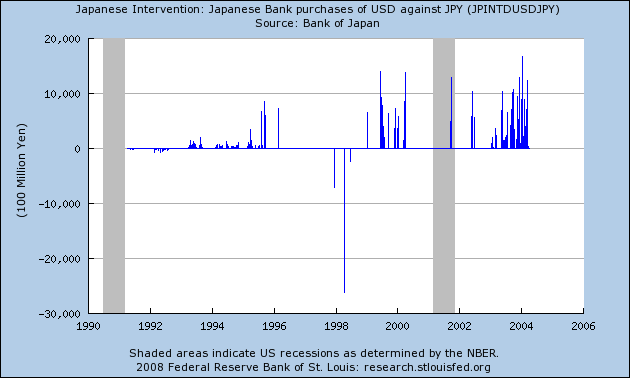

So where does Fujii actually stand? I would personally hazard to guess that his original explication is still the most accurate portrayal of how he will tend to the Yen while in office. The former Liberal Democratic Party (LDP) administration intervened several times while in office (once under the direction of Fujii himself!) and most recently in 1994. Despite spending trillions of Yen, the campaign only marginally stemmed the rise of the Yen.

Meanwhile, the Japanese economy has been mired in what could be termed the “world’s longest recession, dating back to the 1980’s. It’s clear that the cheap-Yen policy, designed to promote exports, hasn’t benefited the Japanese economy. The new administration, hence, has indicated a shift in strategy, away from export dependence and towards domestic consumption.

Ironically, the nascent Japanese economic turnaround is once again being driven by exports. Fujii is no doubt cognizant of this, and doesn’t want to jeopardize the recovery for the sake of ideology. For example, Toyota Corporation has indicated that a 1% appreciation in the Yen against the Dollar costs the company $400 million in operating income. In addition, while a strong Yen increases the purchasing power of Japanese consumers, an overly strong Yen can lead to deflation, as consumers forestall spending in anticipation of lower prices down the road.

In other words, Fujii is certainly not a proponent of Japan’s recent runup, but his stance is more nuanced than initially understood. “Fujii is basically saying currencies should reflect economic fundamentals and that it is wrong to manipulate their moves to lower the yen for the sake of exporters,” offered one strategist. This, the markets finally seem to understand, and the Yen has actually reversed course over the last week. After all, “A yen in the 80s is excessive,” given the context of record low interest rates and a economy that is still contracting.

In the near-term, then, it doesn’t even make sense to talk about intervention. It seems the markets were getting ahead of themselves in this regard. It doesn’t make sense to price out the possibility of intervention when interevention shouldn’t be a factor in the first place. If on the other hand, the Yen continues to appreciate, then Fujii may have consider how fixed his principles really are.